Real numbers from a real villa. 12 months of actual performance from a two-bedroom villa we manage in Bingin — occupancy, margins, expense ratios, and what the owner actually keeps. No projections. No pro formas. The same data we send to the owner each month.

All figures in this article are presented in USD for international readability. Cabo Bali complies with Indonesian currency regulations — all villa rental transactions are priced and settled in Indonesian Rupiah (IDR). USD figures are converted at the IDR bookkeeping rate documented in each monthly owner report.

Written by Keanu Fischell, Co-Founder and Director, Cabo Bali. Last updated June 2026 · 12 min read.

Key Numbers at a Glance

Key Numbers at a Glance

| Metric | Value |

|---|---|

| Annual gross revenue | ~$80,000 |

| Owner profit (after all costs) | ~$44,000 |

| Net yield on $280–330K acquisition | 14–16% |

| Annual occupancy | 96% |

| Average daily rate (ADR) | $221, trending $250+ |

| RevPAR | $215, trending $240+ |

| Direct booking share | 10%, projected 20–25% by end of 2026 |

| Operating expense ratio | 13–20% of net revenue |

| Management fee structure | 13% of gross + 2.5M IDR/month flat admin |

Who This Analysis Is For

You'll get the most out of this article if you're:

- Considering buying a 2-bed villa in Bingin or the wider Bukit Peninsula and want a real benchmark against the projection deck a broker handed you

- An existing owner of a 2-bed villa in Bali wanting to pressure-test whether your current numbers are normal, weak, or strong relative to a comparable property under professional management

- A developer or investor evaluating yield on Bali villas as an asset class and wanting actuals — not pro formas — to anchor your model

If you're looking for a guide to which villa to buy, this isn't that article — this is about what one specific property actually does, month by month, line by line. The buyer's checklist sits separately.

TL;DR

- Annual gross revenue: High $70Ks to low $80Ks

- Owner profit after everything: ~15% net yield on a $280–330K acquisition (range: 14–16% across the acquisition band)

- Owner keeps: 55–60% of gross. 2025 came in at ~55% — already inside the normalised range, without the bad-month adjustments the 1-bed needed

- Occupancy: 96% on available nights, with five months at 97% or higher and three months at a full 100%

- ADR: $221 average in the first 8 months of 2025, trending $250+ through the back half of the year

- Direct bookings: Already running at 1-in-10 bookings via cabobali.com — and they're consistently the highest-revenue bookings of the month

Why We're Publishing This

Every sales deck in Bali shows you a revenue projection. Projected occupancy, projected ADR, projected annual return — all forward-looking, all optimistic, all conveniently free of the months where things go wrong.

This article is the opposite. It's a backward-looking, 12-month performance summary from a single two-bedroom villa we manage in Bingin. Every number from January through August comes from the actual owner report. September through December is modelled on the seasonality pattern of our comparable 1-bed Uluwatu villa — a methodology we'll be transparent about throughout, and which we'll reconcile against the real figures in a Q4 2025 update.

We're publishing it because we think the gap between what buyers are told to expect and what owners actually experience is one of the biggest problems in the Bali villa market. And the fix isn't better projections — it's published actuals.

If you're considering buying a villa in Bingin, or if you already own one and want to benchmark your performance, this is the most honest reference point we can give you.

Who We Are and Why That Matters for This Article

Cabo Bali was founded by villa owners and developers whose background is in Google and performance marketing — not hospitality. We built and invested in our own villas before we managed anyone else's, and we started the management company because the existing options in Bali were failing the asset we'd just spent two years building.

That background shapes everything. Performance marketing trained us to measure what matters — RevPAR, channel mix, conversion rate, cost per acquisition — and to optimise against real data, not gut feel. Villa development taught us what a property actually costs to run when nothing is hidden, and what the difference is between a villa that's been built well and one that quietly leaks margin every month.

Combining those two skill sets is what Cabo actually is: a management company that treats your villa as a financial asset, not a hospitality project.

Every decision in this article — the pricing strategy, the channel distribution, the direct booking investment, the maintenance response — was filtered through one question: does this protect or improve the owner's yield? If it doesn't, we don't do it.

We publish data like this because investment-grade management should come with investment-grade transparency. If your current manager can't show you numbers like these, that gap is worth understanding.

The Property

- Type: 2-bedroom villa

- Location: Bingin, Bukit Peninsula

- Why Bingin: Walkable to the beach path, the warung scene, and one of the most consistent left-handers in the world. Bingin gives you Uluwatu's scenery and surf without the car-dependent isolation that defines the wider Bukit. We think of it as Uluwatu with walkability — and the booking data backs that up

- Management: Cabo Bali

- Channels: Airbnb, Booking.com, Trip.com, direct bookings via cabobali.com

- Pricing: Dynamic pricing via PriceLabs, benchmarked against AirDNA Luxury 4.9★ tier

- Acquisition cost range: $280,000–$330,000

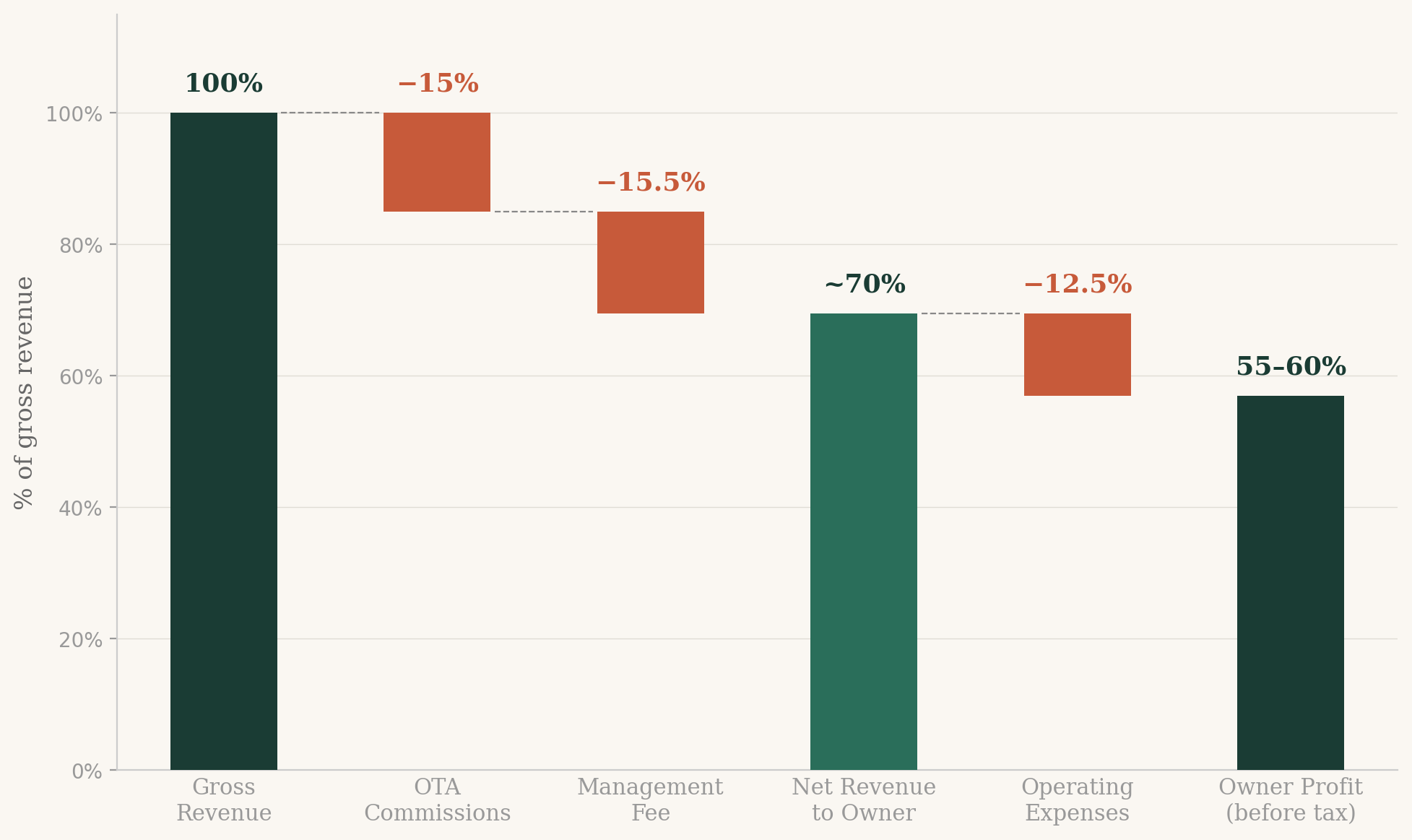

The Full Revenue Waterfall

Here's what happens to every dollar a guest pays — from the gross booking amount down to what the owner actually receives.

Where the money goes (as a percentage of gross revenue)

Where the money goes (as a percentage of gross revenue)

| Category | % of Gross |

|---|---|

| Gross Revenue | 100% |

| OTA Channel Commissions (Airbnb/Booking.com/Trip.com blend) | –13–17% |

| Cabo Bali Management Fee (13% of gross + 2.5M IDR/month flat admin) | –15–16% |

| Net Revenue to Owner | ~70% |

| Operating Expenses (housekeeping, pool, garden, POMEC, staff, maintenance) | –13–20% |

| Owner Profit (before tax) | 55–60% |

A note on our pricing: our management fee is 13% of gross revenue plus a flat 2.5 million IDR per month (~$160) for administrative work — bookkeeping, owner reporting, banking admin, vendor coordination. On a villa at this revenue level, the all-in effective rate lands at 15–16% of gross. The flat admin component slightly compresses owner margin in lower-revenue months and expands it in higher-revenue ones, which we think is the more honest way to price management work that doesn't scale linearly with revenue.

The 55% is the actual 2025 result. The 60% is the upper end of the normalised range once we account for direct booking growth. On a $280–330K acquisition, that translates to roughly 15% net yield annually, with a range of 14–16% depending on where in the acquisition band the villa was bought.

The percentage of direct bookings we drive also directly increases owner margin. Every booking that comes through cabobali.com instead of Airbnb saves the owner 15–17% in OTA commissions on that booking — money that flows straight to the bottom line. On this villa, one direct booking in August generated 27% of the month's revenue from a single guest, saving the owner roughly $225 in commission costs on that stay alone.

The Occupancy Picture

The Occupancy Picture

| Metric | 2025 Performance | Recent Trend |

|---|---|---|

| Nights available (no owner stay this year) | 365 | — |

| Nights occupied | ~352 | — |

| Occupancy | 96% | 97% |

| Average daily rate | $221 (YTD Aug) | Trending $250+ |

| RevPAR | $215 (YTD Aug) | Trending $240+ |

Peak months (January, April, August): 100% occupancy — every available night booked.

Lowest occupancy month: June at 90% — still 20 points above the AirDNA Bukit Peninsula average of 70%, and the only month all year that fell below 96%.

The ADR trend is meaningful. The villa opened the year at $194 ADR in January and climbed through the year as rate positioning strengthened and reviews accumulated — June, July, and August averaged $269 / $278 / $256 respectively. The trailing 3-month ADR sits above $260, which is the level we're underwriting forward expectations against.

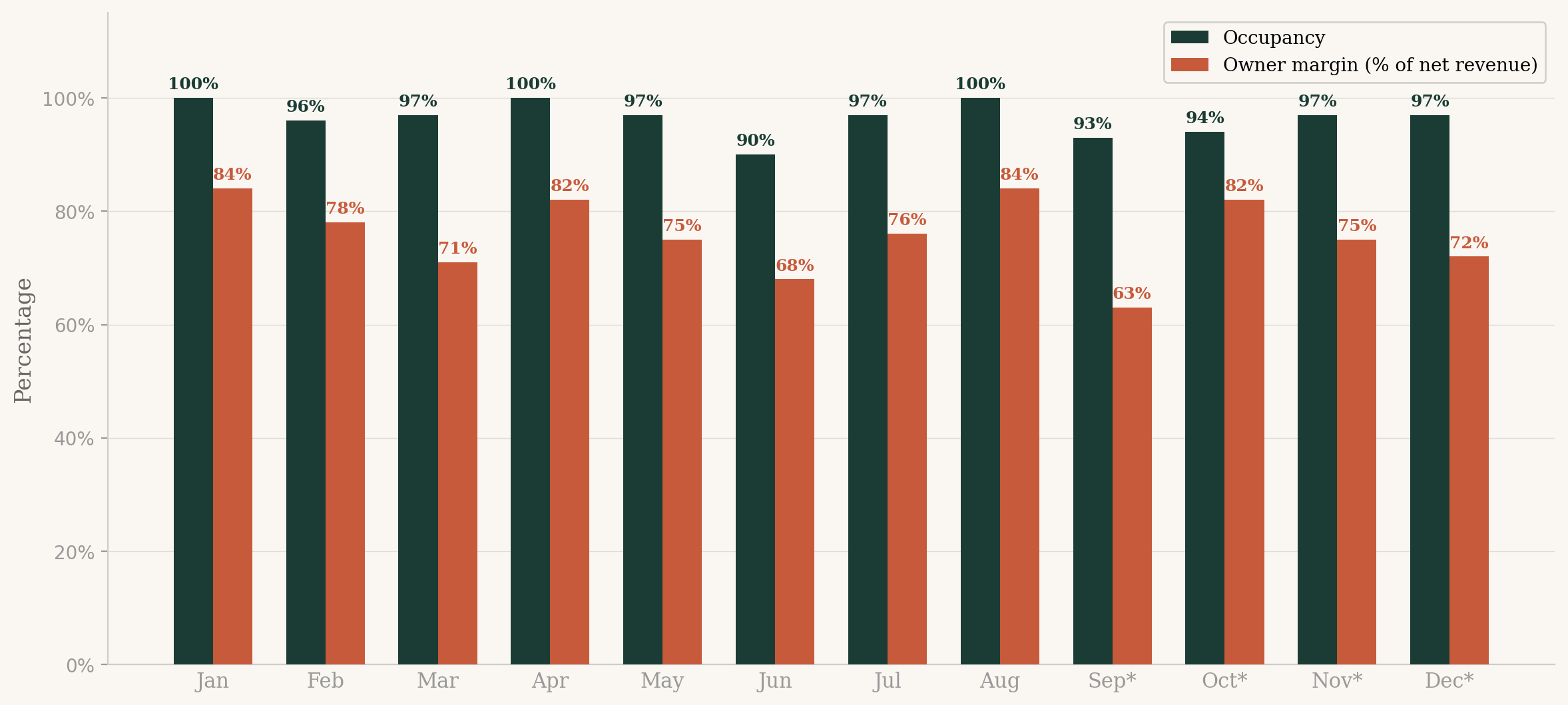

Month by Month: What the Margins Actually Look Like

Rather than dollar amounts, here's what the owner's margin looked like as a percentage of net revenue each month:

Month by month: what the margins actually look like

| Month | Occupancy | Margin | Notes |

|---|---|---|---|

| January | 100% | 84% | Peak season, perfect occupancy |

| February | 96% | 78% | |

| March | 97% | 71% | Lower-rate month, equipment investment |

| April | 100% | 82% | |

| May | 97% | 75% | Shoulder season, rate softens |

| June | 90% | 68% | Only sub-96% month of the year |

| July | 97% | 76% | ADR peaks at $278 |

| August | 100% | 84% | Best margin month, 100% occupancy |

| September* | 93% | 63% | Modelled on comparable 1-bed seasonality |

| October* | 94% | 82% | Modelled |

| November* | 97% | 75% | Modelled |

| December* | 97% | 72% | Modelled, with NYE rate premium |

| Full Year | 96% | 75% |

*September–December figures modelled on the actual seasonality pattern of our comparable 1-bed Uluwatu villa, scaled to this villa's ADR level. Actual figures will be reconciled in our Q4 2025 update once the full year closes.

What the numbers tell you

The good months are predictable and they cluster. January, April, and August all cleared 80%+ margin at 100% occupancy. These are peak-season months where occupancy is locked, rates hold above $190, and nothing unusual hits the expense line.

The expense profile is stable. Unlike the 1-bed we wrote about — which had a pump replacement land in the same month as annual service renewals — this villa hasn't had a single month where expenses spiked above $1,540. The biggest expense category is consistently electricity ($250+ per month), then housekeeping consumables and laundry. There's no maintenance disaster in the data because there hasn't been one. That's what a well-built villa with proactive operations looks like on a P&L.

The only soft month — June at 90% occupancy — wasn't an operational failure. Rate held above $269 ADR through it, and the lower occupancy was a deliberate pricing choice to protect ADR through a known soft window. The margin compression came from elevated maintenance in that specific month, not from rate weakness.

Pro tip for owners. A 2-bed in Bingin earning $80K gross with no maintenance disasters in the year is not the same villa as a 2-bed in the same area earning $80K with two emergency pump replacements baked in. The headline revenue number isn't the asset — the predictability of the margin is. Look at the variance across months, not just the average.

What a Normal Month Looks Like at the Booking Level

To give a sense of the booking rhythm, here's August 2025 in full. The villa booked all 31 available nights across 10 bookings — 100% occupancy. The channel mix included Airbnb (7 bookings), Booking.com (2 bookings), and 1 direct booking via cabobali.com. Average length of stay was 3.1 nights, but the booking pattern was bimodal — five short stays under 3 nights and four longer stays of 4–6 nights.

The standout: a single 6-night direct booking via cabobali.com generated $1,502.77 in gross revenue — 19% of the month's gross from one booking, at a $250.46 ADR that matched the OTA bookings on the same nights. Because it was direct, the owner paid roughly $48 in payment processing instead of the $200+ that an OTA would have charged on the same booking. That's $150+ that flowed straight to the bottom line on a single stay.

Direct bookings are a meaningful part of our channel strategy — they avoid the 15–17% OTA commission entirely, which directly improves owner margin. Building a direct booking channel takes time and brand investment, but it pays back compounding returns once the channel is established. We project direct bookings on this villa to grow from 10% of the channel mix in 2025 to 20–25% over the next 24 months as the property accumulates reviews on cabobali.com and benefits from our portfolio-wide repeat guest base.

The longer stays are where the real yield lives — they reduce turnover costs (fewer cleanings, less amenity refill, less wear on linens) and they reduce the empty-night risk between bookings. A booking calendar with five 6-night stays is operationally easier and more profitable than the same revenue spread across fifteen 2-night stays.

How This Compares to the Market

AirDNA benchmarks the South Kuta/Bukit Peninsula market at:

- RevPAR: ~$55/night

- Occupancy: 70%

- ADR: ~$90/night

This villa runs at:

- RevPAR: above $215 (4× the market benchmark)

- Occupancy: 96% annual

- ADR: $221 average in 2025, trending $250+

The outperformance is real — but it's conditional. This villa is well-built, well-located in the highest-demand pocket of the Bukit, professionally photographed, and actively managed with dynamic pricing and multi-channel distribution. The Bingin submarket itself commands a premium within the wider Bukit Peninsula because of walkability, the surf, and the warung scene — but that premium only converts to revenue with the right setup behind it.

A 2-bed villa in Bingin with average photos, static pricing, single-channel distribution, and reactive maintenance would not produce these numbers. Same neighbourhood, same architecture, same bedroom count — and probably 25–35% less revenue. The location is necessary but not sufficient.

"Amazing team :) amazing house, beautiful design. Best sleep. Will recommend." — Ron, Puntarenas Province, Costa Rica (Google review, August 2025)

The review above is from a guest who stayed at this villa twice in August 2025 — once for two nights and then returned for another two nights five days later. That repeat-within-a-month pattern is part of what makes the booking calendar work: a guest who comes back during the same trip is a guest who skipped the OTA the second time, and that's the kind of behaviour direct booking infrastructure is built to capture.

Why Bingin Specifically Outperforms the Bukit Average

Worth zooming in on this. The wider Bukit Peninsula is a large submarket — it includes Pecatu, parts of Jimbaran, Balangan, Padang Padang, and Uluwatu proper, in addition to Bingin. Within that submarket, the per-village performance varies significantly.

Bingin's specific advantage is walkability. Most of the Bukit is car-dependent — you can't walk to a coffee, you can't walk to dinner, and you can't walk to the beach without driving to a clifftop first. Bingin breaks that pattern. The beach path is a 4-minute walk from most of the village. The warung scene is integrated, not gated. The surf is at the bottom of the cliff steps. For the segment of the international guest who wants the Bukit's scenery without renting a scooter, Bingin is the only viable answer.

That walkability translates to higher booking conversion at higher ADRs. Guests who would normally choose Canggu for the walkable-village reason find their way to Bingin once they discover the format exists in the south. We see this in the booking data — Bingin guests skew slightly older, stay slightly longer, and convert from the listing page at higher rates than equivalent Uluwatu-proper guests.

That's the structural reason a 2-bed in Bingin clears $80K gross while a comparable 2-bed three kilometres away in Pecatu might struggle to clear $55K with identical management.

Why Direct Bookings Change Everything

Most villa management companies in Bali are entirely dependent on OTAs. Every booking comes through Airbnb or Booking.com, every dollar of revenue is subject to their commission, their policies, and their leverage.

That's a problem — and not just because of the 15–17% commission.

OTAs have leverage over your villa. When a guest complains on Airbnb, the platform can issue refunds from your payout without your approval. When Airbnb changes its review algorithm, your ranking can shift overnight. When Booking.com raises its commission rates, you have no negotiating position. The platform owns the relationship with the guest, not you.

Every booking that comes through your own direct channel removes that leverage entirely. The guest pays you directly. The review lives on your terms. The refund decision is yours, not the platform's. And the 15–17% commission stays in the owner's pocket.

This is why we push direct bookings hard. It's not just a margin play — it's a risk-reduction strategy. The more of your revenue that flows through your own channel, the less exposed you are to platform decisions that you didn't make and can't influence.

We invest in building each villa's direct booking presence through cabobali.com — professional listing pages, direct booking incentives (guests save vs OTA pricing), and a guest experience that drives repeat bookings into our own channel rather than back to the OTAs that originally drove them. On this villa specifically, the 10% direct booking share in 2025 represents roughly $8,000 of annual gross revenue that would otherwise have flowed through Airbnb. The commission saving on that volume alone is $1,200–1,400 per year of pure owner margin.

Pro tip for owners. Ask your management company what percentage of your bookings come through direct channels. If the answer is zero — or if they don't have a direct booking channel at all — every dollar of your revenue is exposed to OTA platform decisions you can't influence. That's not a management strategy, that's a vulnerability.

What Most Sales Decks Get Wrong

If a broker showed you this villa before purchase, their sales deck would probably have projected 80% occupancy at $200 ADR, with expenses hand-waved at "approximately 20% of revenue." That would give you a projected gross of $58,400 and a projected owner profit of ~$46,700 — translating to a "projected 15% net yield" on a $310K acquisition.

The headline net yield number would, by coincidence, be roughly right. But the inputs would be completely wrong. The villa actually delivers a higher gross ($80K vs the projected $58K) because the broker understated both occupancy and ADR. The expense ratio is genuinely 13–20% of net revenue (not 20% of gross), and the OTA and management commissions — which the broker probably forgot to include at all — add another 28–30% of gross. The actual profit math works out to a comparable net yield, but for entirely different reasons than the deck claimed.

This is why we publish real numbers. Not to discourage investment — the returns here are genuinely strong at 14–16% net yield. But to set the expectation correctly so that year one doesn't feel like a disappointment when the gross revenue is bigger than projected but the expense line is also bigger, and the owner has no framework for understanding whether that's normal.

Pro tip for buyers. Ask your broker to show you performance data like this — 12 months, occupancy and margins, the bad months included. Not a projection. Not a model. Actual historical performance from a comparable villa under professional management. If they can't produce it, that's the signal — not the sales deck they hand you instead.

The Bear Case: Why ADR Could Soften — And Why This Villa Should Defend

We've made the bull case above. Honesty requires the bear case too.

The Bukit Peninsula has seen a significant supply build over the past three years. New villa listings are coming onto Airbnb and Booking.com every month. Several developers are completing multi-unit projects in Pecatu, Uluwatu, and Bingin itself. Bali tourism arrival numbers are growing, but listing supply is growing faster on some submarket views — which is the textbook setup for ADR compression.

If supply outpaces demand growth and the average Bali villa ADR softens by 15% over the next 24 months, here's what that would do to the numbers on this villa, holding occupancy at 96% and the cost base broadly stable:

What if rates drop?

Holding occupancy at 96% and cost base broadly stable

| ADR Change | Annual Gross | Owner Profit | Yield on $280K | Yield on $305K | Yield on $330K |

|---|---|---|---|---|---|

| No change | $80,000 | $46,500 | 16.6% | 15.3% | 14.1% |

| –10% | $72,000 | $40,600 | 14.5% | 13.3% | 12.3% |

| –15% | $68,000 | $37,700 | 13.5% | 12.4% | 11.4% |

| –20% | $64,000 | $34,700 | 12.4% | 11.4% | 10.5% |

| –25% | $60,000 | $31,800 | 11.4% | 10.4% | 9.6% |

The honest takeaway: even at a 25% ADR compression — which would be a significant market correction — this villa still delivers ~10% net yield at the top of the acquisition band, and ~11% at the bottom. That's still above the unleveraged return on most emerging-market real estate.

But — and this is the important part — that compression scenario assumes this villa softens at the average rate. It probably wouldn't.

This villa is not your average copy-and-paste 2-bed in Bingin. A meaningful portion of the new supply on the Bukit is exactly that: identical-floorplan units, hand-rendered marble counters that look great on a render and chip in six months, no thought given to acoustic separation between bedrooms, contractor-grade fittings dressed up for a listing photo, and zero design specificity. Those properties exist to be listed and to fill — they don't exist to defend a rate position when supply increases.

A well-designed, well-located, well-built villa with a five-figure quarterly review velocity, multi-channel distribution, dynamic pricing, and a direct-booking channel that compounds over time defends differently. It loses the bottom of the market first — the rate-shoppers who'd happily switch to a cheaper unit — and keeps the top, where guests are choosing the property on aesthetic, location, and review signal, not on dollar-saved-per-night.

The villas that get hurt in a supply correction are the ones that were always pricing on equivalence. The villas that defend are the ones that were always pricing on differentiation. This villa is built and managed for the second category.

Pro tip for buyers. Don't underwrite a Bali villa investment on the assumption that 2025 ADRs hold flat forever. They probably won't. Underwrite at a 15–20% compression scenario and check what the numbers do there. If the deal still works at –20% ADR, you have margin of safety. If it only works at flat — you're betting on no supply growth in one of the most actively developing tourism submarkets in the world.

Why the Forward Numbers Should Be Stronger

Three things that should improve in 2026:

- ADR maturation: The villa opened 2025 at $194 ADR in January. By the back half of the year it was averaging $260+. Annualising 2026 at the trailing 6-month ADR rather than the YTD ADR moves the gross revenue baseline up by roughly $10–12K

- Direct booking growth: 10% direct in 2025, projected to 20–25% by end of 2026. Every percentage point shift from OTA to direct adds roughly $130 of margin per year on a villa at this revenue level. A 15-point shift is $2,000 of pure additional yield

- No owner stay deduction: This villa had a full 365 nights available in 2025 — no owner stay reduced the revenue baseline. If that pattern holds, no recalibration needed; if owner stays do happen in 2026, they'll deduct from the revenue line but not from the underlying property performance

The forward picture is a high $80Ks to low $90Ks gross, with profit margins consolidating in the 56–60% range as direct booking share grows. That's a 15–17% net yield range on the same acquisition band.

Key Takeaways

Key takeaways

- This 2-bed in Bingin ran 96% occupancy on 365 available nights in 2025 — roughly 26 points above AirDNA’s ~70% Bukit Peninsula benchmark.

- It earns about $80K gross, leaving the owner roughly $44K profit (55–60% of gross) — around 14–16% net yield on a $280–330K acquisition.

- ADR averaged $221 in 2025 and is trending past $250; RevPAR (~$215) runs about 4× the AirDNA Bukit benchmark.

- Even modelling a 25% market-wide ADR correction, the villa still clears ~10–11% net yield — the margin of safety buyers should underwrite to.

- Direct bookings (~10% today, projected 20–25%) are the highest-margin channel — every direct stay saves the owner 15–17% in OTA commission.

- Outperformance is conditional: location is necessary but not sufficient. Cabo manages 20+ villas at 91% average occupancy and 4.85/5 from 500+ reviews.

Definitions Used In This Article

- ADR (Average Daily Rate): Total gross revenue divided by the number of nights occupied. The headline rate per booked night.

- RevPAR (Revenue Per Available Room/Night): Total gross revenue divided by the number of available nights (including unoccupied ones). The truer measure of property performance because it combines rate and occupancy into one number.

- Occupancy: Percentage of available nights that were booked. We report on available nights — owner-stay nights are excluded from the denominator because they were never on the market to be booked.

- OTA (Online Travel Agency): Booking platforms like Airbnb, Booking.com, and Trip.com that bring guests to the villa in exchange for a commission, typically 13–17% of gross.

- Net Revenue: Gross revenue minus OTA commission and management fee. This is what flows into the villa's operating account.

- POMEC (Property Operations, Maintenance and Energy Costs): The line item that covers electricity, water, pool chemicals, garden upkeep, and routine maintenance. Roughly 4–7% of gross revenue for a well-run 2-bed villa in Bali.

- Net Yield: Annual owner profit (after every cost — commissions, management, operations) divided by the villa's acquisition cost. The cleanest single number for comparing a villa investment to other asset classes.

- Channel Commission: The fee the OTA charges per booking. Airbnb is roughly 16–17%, Booking.com is roughly 13–15%, Trip.com varies by booking.

FAQ

What if the Bali villa market gets oversupplied and ADRs drop?

It's a real risk and we model for it. At 15% ADR compression with occupancy held, this villa still delivers 12–14% net yield across the acquisition band. At a 25% compression — which would be a meaningful market correction — it still delivers 10–11% net yield. But the modelling assumes the villa softens at the average market rate, which it probably wouldn't. Properties built and managed for differentiation defend rate in supply corrections. Properties built for equivalence don't. The villa this article describes is in the first category.

Is 15% net yield realistic for a 2-bed in Bingin?

On a $280–330K acquisition with proper management, yes. This is actual 8-month performance plus a transparently-modelled Q4. Even with the conservative Q4 projection — which uses a comparable 1-bed's softer Sep-Dec pattern — the villa delivers 14–16% net yield depending on where in the acquisition band the villa was bought.

Why publish projected figures instead of waiting for the full year?

Because the owner reports are real and the seasonality model is transparent. The Jan-Aug numbers are actual; the Sep-Dec numbers use the documented pattern of a comparable property as a placeholder. We'll publish a reconciliation in early 2026 with the actual full-year figures replacing the projection. Anyone can audit the methodology in real time.

What's the management fee structure?

13% of gross revenue plus a flat 2.5 million IDR per month (~$160) for administrative work. On a villa at this revenue level the all-in effective rate is 15–16% of gross. The flat admin component prices the work that doesn't scale linearly with revenue — bookkeeping, owner reporting, banking admin — separately from the variable revenue management component.

Why is Bingin's performance stronger than the wider Bukit Peninsula?

Walkability, the surf, and the warung scene. Bingin is the only walkable village on the Bukit Peninsula, and that single attribute pulls in a guest segment that would otherwise default to Canggu or Seminyak. Higher booking conversion at higher ADRs is the result.

Did the villa have any owner stays in 2025?

No. The villa ran 365 nights available all year. The Cabo policy on owner use is no restrictions and no commission — but in this case the owner didn't use the villa in 2025.

What channels generate the bookings?

Airbnb, Booking.com, Trip.com, and direct bookings via cabobali.com. The direct channel currently represents about 10% of bookings and is growing. We actively build it because every direct booking saves the owner 15–17% in OTA commissions — pure margin improvement.

What would more direct bookings do to the margin?

Significant impact. Shifting from 10% to 25% direct over 24 months adds an estimated $2,000+ per year to net owner profit at this revenue level. This is one of the highest-leverage things a management company can do for an owner that doesn't require capex.

Is this villa's performance typical of Cabo's portfolio?

Yes. We manage villas at 91% average portfolio occupancy with a 4.85/5 guest rating across 500+ stays. This villa sits above the portfolio average on occupancy and inside the typical range on margin — strong, but not an outlier.

If You Own a Villa in Bingin

If you're reading this and your 2-bed isn't hitting these numbers, the question isn't whether the market supports it — it does. The question is what's holding your villa back: pricing strategy, photography, channel mix, operational discipline, or maintenance reactivity. Usually it's some combination of the five.

We're happy to look at your current performance and give you an honest read on where the gap is. No pitch. No pressure. Just the data.

About the author. Keanu Fischell is co-founder of Cabo Bali, which manages 20+ boutique villas across Uluwatu, Bingin and Canggu. He writes from the operator's side of Bali villas — real numbers, real guest feedback, and lessons from running the portfolio day to day.

Related reading:

- How Lago Villas Beats the Luxury Benchmark in Bingin — With Construction Next Door

- What a 1-Bed Villa in Uluwatu Actually Earns (2026)

- How Much Does Bali Villa Management Cost? A Full 2026 Breakdown

- The Top 10% of Villas in Uluwatu: What Cabo Bali Is Doing Differently

- How to Choose a Villa Management Company in Bali

Sources & References

Performance figures come from Cabo Bali’s own monthly owner reports: January–August 2025 are actuals, and September–December 2025 are modelled on the actual seasonality pattern of a comparable 1-bedroom Uluwatu villa we manage, scaled to this property’s ADR level. All figures are presented in approximate USD for international readability. Market baselines and the metric definitions used here are drawn from the authoritative industry, government and platform sources below; AirDNA South Kuta/Bukit Peninsula data is current as of April 2026. As a reference point, AirDNA’s island-wide data puts average Bali short-term-rental occupancy in the mid-40% range and the Bukit submarket near 70% — the benchmarks this villa’s 96% is measured against.

- AirDNA — short-term-rental market data (RevPAR, occupancy and ADR baselines for Bali and the Bukit Peninsula).

- BPS Bali (Badan Pusat Statistik Provinsi Bali) — official Bali foreign-tourist arrival statistics.

- Bank Indonesia — official IDR reference exchange rates used for USD conversion.

- Horwath HTL — Indonesia hotel and tourism market reports.

- Colliers Indonesia — Bali and Indonesia property market research.

- STR (CoStar) — global hospitality benchmarking and the standard definitions of ADR, occupancy and RevPAR.

- Airbnb Help Center — host service-fee structure.

- Booking.com Partner Hub — commission model.

- PriceLabs — dynamic-pricing methodology referenced for rate setting.

- Wheelhouse — short-term-rental revenue-management benchmarks.

- Bali Hotels Association — island-wide occupancy and tourism commentary.